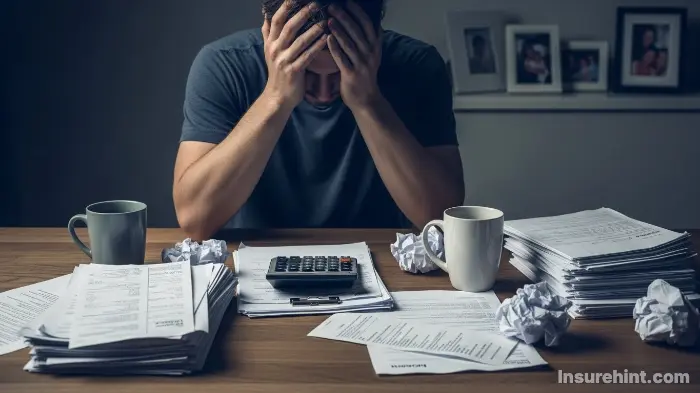

When will workers’ comp offer a settlement? This question is always on your mind. You are injured and are unable to work. The bills are piling up fast. Your family is completely dependent on you.

The waiting is unbearable and long. You need answers right now. This is the exact stress that most injured workers feel.

Here is the truth you need. Settlement offers are usually provided following certain milestones. The insurance company goes through a calculated process.

It gives you power to understand this timeline. This knowledge helps you to prepare for negotiations. It also lessens your anxiety by a long stretch.

This is a very detailed guide and spells it out well. You will get to know about each phase. You will know what causes settlement offers.

We are going to cover medical improvement stages. Our team will describe impairment ratings in detail. Furthermore, we will unveil negotiation strategies that work.

By the end of this article, everything becomes clear. You will know exactly what you will get. You will be ready for all of your steps.

The Reality of Workers’ Compensation Settlements

Workers’ compensation is there to protect the injured employee. It is where medical care and wage replacement is offered. The system has specific rules and time lines.

However, insurance companies are businesses first. They want to reduce the amount of payout as much as possible. This causes some tension in each claim.

Your employer has affordable business insurance for this purpose at an affordable price. The insurance company goes directly through your claim. They regulate the process of the settlement offer.

Settlements make claims final in most cases permanently. The insurance company likes predictability. They want to avoid having ongoing obligations to make payments.

You have to know their motivations clearly. This knowledge helps you to negotiate better. It warms you up to their tactics.

According to the U.S. Department of Labor, the rules of the workers compensation differ from state to state. Each of the states has different timelines and requirements. This has an impact when offers are made.

Understanding When Will Workers’ Comp Offer a Settlement: The MMI Rule

When will workers’ comp offer a settlement usually depends upon MMI. MMI is an acronym for Maximum Medical Improvement. This is the golden rule of settlements.

MMI is an important medical determination. It means that your condition has become stable. Further treatment will not make you any better.

This is up to your treating physician to make this determination. They assess your current status in terms of health. They determine if you have hit a plateau.

Insurance companies are waiting for MMI to settle. They have to calculate the total claim value. They cannot do this while being treated.

“Insurance adjusters almost never offer settlements before MMI. They need certainty about the total claim value. Rushing to settle before MMI often hurts injured workers.”

— Attorney Mark Davidson, Workers’ Compensation Specialist

This makes perfect business sense for insurers. Settling too soon is risky financially. They may pay less than they need to pay.

On the other hand, they may end up paying more than their due. Neither outcome is in their own best interests. MMI gives them the certainty that they need.

📊 The MMI Timeline Chart

Timeline Phase 1: Reporting Your Workplace Injury

The settlement timeline is based on the start of reporting of injury. This first phase is absolutely critical. Mistakes in this area hold everything up considerably.

Most states mandate the immediate reporting of injuries. Usually you have a 30 day max. Some states demand even quicker notification.

OSHA – Requirements for employers in reporting certain things Serious injuries need to be reported promptly. This leaves trails of documentation of claims.

Your employer shall file required paperwork. They advise their workers compensation insurance carrier. The insurance company initiates a claim file.

Proper Documentation Accelerates the Process

Good documentation makes for faster settlement offers. The insurance company requires all information. A lack of details leads to avoidable delays.

Here is what you must document:

- Exact date, time and place of injury.

- Names of witnesses at time of incident.

- Detailed description of the way injury was sustained.

And this information becomes the basis of your claim. It helps to clearly establish liability. It is faster than the entire process.

Medical records are extremely important in this phase. See a doctor once you have been injured. Get anything written up in writing.

Your employer can refer you to certain doctors. These are often referred to as “panel physicians.” Follow his or her instructions at first.

When Will Workers’ Comp Offer a Settlement During Phase 1

When will workers’ comp offer a settlement during this early phase? The truthful answer to this is almost never. The first phase, phase 1 is all about making your case.

Insurance companies are collecting information right now. They are not prepared to discuss settlements. They are testing the validity of the claims first.

Adjusters investigate the incident thoroughly in this time. They interview and review documentation of witnesses. They decide whether the claim is legitimate or not.

This phase usually lasts a period of two to four weeks. Complex cases may take a longer time. Simple cases go through processing faster.

Don’t expect the settlement discussion yet. Establish proper procedures and focus on following them instead. This foundation is important for future negotiations.

Understand the claims process to assist with other insurance issues. For example, State Farm life insurance claims are no different in their understanding.

Timeline Phase 2: Treatment and Wage Replacement Benefits

The second phase is active medical treatment. Your worker’s compensation benefits start flowing. The insurance company makes direct payments for medical bills.

You are also given wage replacement benefits now. These are known as temporary disability benefits. They make up partially for lost income.

Temporary Total Disability or TTD is most common. This applies when you are not able to work at all. You get a percentage of your average wage from each week.

Temporary Partial Disability (TPD) is another matter. This includes reduced work capacity situations. You work limited hours do lighter duties.

Medical Treatment Continues Until Stabilization

Your doctors offer continuous medical care. Treatment is aimed at maximum recovery possible. In some cases surgery may need to be done.

Physical therapy is prescribed in most cases. Pain and inflammation are controlled using medications. Specialists offer specialized treatment methods.

Treatment is closely monitored by the insurance company. They may order Independent Medical Examinations. These are referred to as IMEs in the industry.

IMEs involve doctors that the insurer selects. These doctors assess how you are on your own. Their opinions can have a great impact on your claim.

Keep going to all the medical appointments on time. Strictly follow the doctor recommendations. Non-compliance with your claim can hurt it dearly.

Just as proper documentation is important here, it is important where there is professional liability insurance claims as well.

How Treatment Duration Affects Settlement Timing

When will workers’ comp offer a settlement depends on treatment duration to a large extent. Longer treatment times mean longer waiting times.

Insurance companies are unable to accurately calculate settlement values. They need to know total medical costs. Ongoing treatment makes this impossible.

Treatment may last for months or even years. Back injuries often take a long time to rehabilitate. Brain injuries require long term specialized care.

The adjuster assumes responsibility for observing your treatment progress on a regular basis. They communicate with the treating physicians. They want to know when MMI comes near.

Some of the injuries never heal fully or recover. Permanent damage can only be seen with time. This has a big impact on settlement calculations.

Your patience during this phase is very essential. Rushing the treatment is killing your long-term recovery. It also decreases potential settlement values.

Timeline Phase 3: Reaching Maximum Medical Improvement

Phase 3 is the time that settlement discussions really begin. Your doctor says that you have hit MMI. This initiates the settlement consideration process.

MMI does not mean that you are totally healed. It means that your condition is stabilized for good. Further improvement is not medically anticipated.

As per Investopedia Settlement values are based on long-term prognosis. MMI makes this critical information obvious. It is able to give accurate future cost projections.

The Impairment Rating Evaluation Process

After MMI, an impairment rating is given to you. This rating measures how badly you have a permanent disability. It has a significant impact on the amount of settlement offered.

Standardized guidelines are usually used to obtain impairment ratings. The AMA Guides to Permanent Impairment is not unusual. Doctors give percentage ratings to injuries.

For example, the impairment rating of 15% indicates significant disability. A rating of 5% is minor permanent effects. These numbers have a direct effect on calculations of settlements.

The higher the impairment ratings, the higher the settlement offer. The insurance company uses these numbers responsibly. They calculate future benefit obligations very accurately.

The impairment rating is arguably the most important number in your entire workers’ compensation case. It directly determines the settlement value range.

— Attorney Sarah Mitchell, Board Certified Workers’ Comp Attorney

When Will Workers’ Comp Offer a Settlement After MMI

When will workers’ comp offer a settlement after you reach MMI? Of course, usually two to eight weeks. Some cases take more time according to the complexity.

The adjuster goes through your entire medical file. They have all past medical expenses paid reckoned. These experts calculate future medical care costs.

They also calculate permanent disability benefits due. This rating is based on your impairment rating. State formulas are used to determine exact amounts of benefits.

Settlement offers follow these calculations that are done. The insurance company does the first offer. This initial offer is almost always low.

Understanding this timeline is important to you when you are planning financially. Similar planning applies to decisions regarding term life insurance decisions. These both require understanding long-term financial implications.

⚖️ Settlement Negotiation Steps

Doctor confirms your condition has stabilized permanently.

Physician assigns permanent disability percentage rating.

Insurance company makes first offer. Usually 30-50% below fair value.

You or your attorney respond with higher demand.

Both parties agree on final settlement amount.

Why the First Settlement Offer Is Always Low

Insurance companies are profit driven businesses at the most basic level. Their objective is the minimization of claim payouts. This impacts their initial offer strategy.

The first offer puts to the test your desperation level. He or she knows that you are financially stressed. They hope you will accept a low amount soon.

Studies show that initial offers are normally 30-50% below fair value. Some offers are even lower than that. This is normal insurance industry practice.

Understanding the Insurance Company’s Calculation Method

Insurance adjusters have certain formulas when they do the calculations. They take into consideration your medical costs that were already paid. These professionals are responsible for estimating the future medical care needs.

They calculate the permanent disability benefits that are due. Your lost wage claims are also taken into consideration. Furthermore, they account for possible litigation costs.

Then they cut this number down considerably. They consider themselves less than their own calculations. This makes opportunities for negotiating strategically.

You have to know about this game clearly. Accepting the first offer is almost invariably a mistake. It leaves a lot of money on the table.

Just like you would compare car insurance cost options for car insurance, you should give careful evaluation to settlement offers.

Factors That Increase Settlement Offer Amounts

There are several things that can contribute to a bigger settlement value for you. It helps you to prepare properly if you understand these. They also help you negotiate effectively.

Key factors include:

- Severity and effects (permanency) of your injury.

- You pre-injury wage level and your earning capacity.

- Quality of medical documentation, evidence.

Strong evidence of liability increases provides too. If the employer was clearly negligent, the settlements increase. If there were any safety violations, the values go up ever more.

The extent to which you are willing to litigate makes a big difference. Insurance companies have tremendous fear of trial costs. They settle higher in order to avoid litigation expenses.

An attorney’s presence usually will bump up settlement amounts. Studies show attorney represented claimants get more. The increase is normally in addition to attorney fees paid.

The Negotiation Process: Back and Forth Communication

Negotiation is where the amounts of settlement are increased to a huge extent. This is a phase that requires patience and strategy. Most claims are settled during this process.

You make your response to the initial offer in a formal manner. You have the option to accept, reject or counter-offer. Counter-offering is almost always suggested.

Your counter-offer should be well justified. Provide documentation to your demands. Explain why you should be receiving more money.

The counter-offer is reviewed by the insurance company. They usually reciprocate with another offer. This back and forth goes on until agreement.

When Will Workers’ Comp Offer a Settlement Increase

When will workers’ comp offer a settlement increase for negotiations? After you make a good counter-offer; Strong evidence leads to the higher offers.

The adjuster carefully scrutinizes your counter-offer. They take into consideration supporting documentation. These professionals graph litigation risk in the event of no settlement.

They also appreciate your status of representation. Attorneys involvement is often causing higher offers! Adjusters take attorney represented cases more seriously.

Negotiations can last weeks if not months. Complex cases take longer to solve. Simple cases can resolve themselves in a short period of time.

Be patient but also be persistent. Follow up with the adjuster on a regular basis. Keep the negotiation momentum going.

Never accept the first offer. In my twenty years of practice, I have never seen a first offer that was fair. Always negotiate for more.

— Attorney James Rodriguez, Workers’ Compensation Trial Lawyer

Mediation as a Settlement Tool

Sometimes negotiations become completely stalled. Both sides will not move from their position. Mediation can overcome this deadlock in an effective way.

Mediation involves a third party that is not involved in either side. This is a mediator that helps conduct settlement discussions. They facilitate agreement between both sides.

Many states have pre-trial mediation. It is cheaper than litigation significantly. It is also a faster process than going to the court.

Mediators often are retired judges or attorneys. They know the workers compensation law in depth. They are able to objectively evaluate case strengths.

There are quite high rates of success in mediation. Most cases that are mediated do settle successfully. This obviates costly and time-consuming trials.

Now you can think of this process is just like buying temporary car insurance. You need the proper solution to your particular situation.

Finalizing the Settlement: The Compromise and Release Agreement

If both parties have agreed on the amount of settlement, documentation starts. The legal document of formal agreement is referred to as Compromise and Release. Different states use different terminology.

The document is legally binding and permanent. It closes your workers compensation claim for good. It is not possible to reopen the claim later typically.

The agreement sets the amount of exact settlement. It outlines what exactly does the payment cover. It provides any continuing obligation or exclusion.

Critical Elements of Settlement Agreements

Review settlement agreements extremely carefully before signing. Key elements that you need to pay close attention to The mistakes here are usually irreversible.

The amount of settlement should be clearly mentioned. Payment timing should be stated very clearly. Any organized payment terms require documentation.

Future provisions of medical care are important. Some of the settlements close out medical benefits altogether. Others leave medical benefits open to treatment.

Medicare considerations are very important today. Medicare Set-Asides (MSAs) could be required. These are to protect Medicare’s interests in your settlement.

When Will Workers’ Comp Offer a Settlement Finalization

When will workers’ comp offer a settlement no finalization after agreement is reached? Most of the time in two to six weeks.

The insurance company writes up the formal agreement. Their attorneys present all the terms for a settlement. The document is sent to you for your review.

An attorney should see this document. Even if you negotiated alone, get some legal review. This can protect your interests to a great extent.

After signing, the agreement goes for approval. Many states require some administrative or judicial approval. A judge or commissioner is responsible for reviewing the settlement.

Approval makes the settlement fair. It safeguards injured workers against poor settlements. It’s also to make sure that the proper procedures were followed.

With approval the payment processing starts immediately. It usually takes 30 days for you to get paid. Some states have shorter timelines for payment.

Attention to detail is similar with choosing motorcycle insurance. Both cases must carefully reviewed in terms of documentation.

⚠️ Settlement Red Flags to Watch For

Types of Workers’ Compensation Settlements

Two main types of settlement are available in workers compensation. It helps you to make informed decisions if you understand both. And each has distinct advantages and disadvantages.

Stipulated Findings and Award Settlements

This type leaves the case partly open. You receive benefits that have been agreed upon, over a period of time. Future medical care is usually still available.

If your condition gets worse you can go to modification. Continuous protection is provided this way by the settlement. It provides flexibility for medical situations that are not known.

However, administrative burden persists with this type. You are still linked with the workers compensation system. Continuous reporting can be the case.

This option is suitable for workers who have unclear prognoses. It provides protection from unplanned medical complications. It provides safety net for the future needs.

Businesses with commercial auto insurance know the concepts of similar ongoing coverage.

Compromise and Release Settlements

This type of closure is a complete and permanent closing of your claim. There you receive a lump sum payment. All benefits in the future are waived generally.

You accept complete responsibility for the future medical needs. The insurance company is under no further obligations. The case is passed on forever.

This option has certainty and finality. You have all the control over the use of money. You are free to invest or spend as you need.

However, it is very risky as well. If you condition gets worse, there are no further benefits. Medical costs are now your own.

This option is for people who are working in stable conditions. It works when the medical needs in the future are predictable. It has the advantage of enabling independence from the system.

Understanding these differences is of great importance. It has an impact on your financial security in the long run. Pick out carefully in accordance with your situation.

Should You Hire a Workers’ Compensation Attorney?

This question should be seriously considered at all times. Attorneys represent useful knowledge and security. However, they also cost money.

Workers compensation attorneys are usually contingency workers. They get a percent of your settlement. This percentage is normally 10-20% in most states.

Studies continue to demonstrate that attorney representation increases settlements. The increase normally exceeds the fee charged by the attorney. Net proceeds are usually better with representation.

When Attorney Representation Matters Most

There are certain situations which greatly support an attorney’s hire. Denied claims certainly have the advantage of legal representation. Complex medical cases need experienced advocacy.

Disputes on impairment ratings require an attorney’s involvement. Disagreements about disability levels need to done with the expertise. Employer retaliation situations require the protection of the law.

Large potential settlements are a clear justification for attorney costs. The stakes are too high for making mistakes. Professional advice can save your interests.

Simple, straightforward claims may not require the services of attorneys. Small settlements where liability is easy to determine settle easily. Cooperative insurance companies can conduct fair dealing.

However, even straight forward cases do benefit from consultation. Many lawyers will hold free consultations. Use these to evaluate the situation of you.

Just as you would research Humana dental insurance options thoroughly, you should research attorney options thoroughly.

Common Delays in the Settlement Process

Several factors are common causes of delay in settlement offers. By knowing them you can have your real expectations under control. They also help you to avoid delays that can avoided.

The delay in medical treatment has a direct effect on the timing of settlements. If treatment does not stop, settlements cannot be made final. immunosuppressive, encourage regular medical advances where possible.

Disputed liability makes the whole process slow down. If the employer does not agree with your claim, things take time. It takes a lot of time to investigate and hold hearings.

How to Avoid Unnecessary Settlement Delays

Always be consistent in following all the medical appointments and recommendations. Document everything very well and thoroughly. Actively respond to insurance company requests.

Provide information that has been requested, immediately, when asked. Complete all necessary paperwork correctly. Follow up regularly on things that are pending.

Communicate clearly with the insurance carrier of your employer. Maintain professional relationships in the process. Avoid antagonistic interactions, if possible.

Remember to carefully keep copies of all correspondence. Note dates and time of all communications. This documentation is useful in negotiations.

Understand that there are inevitably some delays. Complex injuries take a long time to treat. Some investigations will take longer than expected.

Insurance processes also have their timelines. Adjusters deal with several claims at a time. Patience is also extremely important throughout this journey.

Similar organizational skills are useful when comparing United Healthcare insurance options as well.

State-Specific Variations in Settlement Timelines

The laws regarding worker’s compensation differ greatly from state to state. This has a significant impact on timing the settlement. Understanding the rules of your state is of great importance.

Some states have shorter statute of limitation. Others provide a longer period of time in which to file claims. These deadlines directly impact on the urgency of settlement.

State benefit formulas are also significantly different. The benefits are more generous in some states. Others are restrictive in that they have caps and restrictions.

How State Laws Affect When Will Workers’ Comp Offer a Settlement

When will workers’ comp offer a settlement varies greatly from state to state. Some states promote early settlements actively. Others have timelines that are extended in their processes.

California has specific settlement procedures and requirements. Texas has the option to opt out for coverage. Florida has rigid time frames for different steps.

Research the workers compensation laws of your particular state. State agencies offer useful information on the Web. It is good to know local rules, which will contribute to effective planning.

Consider consultation with a local attorney always. They know the requirements of your state. They can offer general advice in your situation.

Owners of classic car insurance know about state-specific requirements in the same way.

Protecting Your Rights Throughout the Process

The protection of your rights requires protection at every step. There are rules for the workers compensation system. These rules are for protecting injured workers specifically.

Never sign documents that you are not completely clear on. Get the meaning of any confusing words. Ask questions till you are sure you understand.

Do not give recorded statements without being prepared. Adjusters of the insurance might use statements against you. Consider the use of an attorney at statement.

Key Rights Every Injured Worker Should Know

You have the right always to medical treatment. The insurance company will have to pay for reasonable care. Disputes can be taken up through proper channels.

You shall be eligible to disability benefits. These are benefits that cover the lost wages. Calculations should be according to state formulas accurately.

You are entitled to appeal of denied claims. There are administrative processes in dispute. Contested cases are heard by judges/commissioners.

You have the right to always represent a legal representation. Attorneys can help to protect your interest. Fees are regulated by state laws.

Conclusion

Knowing when will workers’ comp offer a settlement is liberating. This knowledge helps you to reduce your stress significantly. It helps you to plan for your future effectively.

The basis of the timeline depends on the attainment of Maximum Medical Improvement. The amount of your impairment rating has a direct impact on the amount for which you are awarded in a settlement. Patience in the treatment process is a safeguard to the value of your claim.

Initial offers of settlement are usually low and insufficient. Negotiation is expected and required for fair results. Consider the use of attorney representation on complicated claims.

Document everything all the time you have your claim process. Take and take up all medical recommendations and give all appointments. Respond promptly to requests from insurance companies always.

Your financial security is dependent on you handling this properly. Take your time and make well informed decisions. Do not pressured by financial pressure to make rush decisions.

When will workers’ comp offer a settlement is predictable by way of proper knowledge. Now you have an idea what the timeline and process is. Apply this knowledge in order to protect your rights and maximize your value of your settlement.

Frequently Asked Questions

How long after MMI will I receive a settlement offer?

After reaching Maximum Medical Improvement, it takes, on average, two to eight weeks for settlement offers to come in. The insurance company requires the time to determine the value of your claim. Complex cases may take longer time. Your impairment rating has a major effect on this timeline and the final amount of an offer.

Can I negotiate a workers’ compensation settlement myself?

Yes, you can do the negotiation without an attorney legally. But according to studies attorney represented claimants are awarded higher settlements typically. Consider your case complexity and potential case value, or the potential settlement value, carefully. Free consultations help you determine whether it is worth your while to represented in your particular circumstances.

What happens if I reject the settlement offer?

Rejecting a settlement offer only continues the negotiation process as normal. You can make a counter-offer accompanied by supporting documentation. If negotiations break down totally, there is mediation or hearing. You don’t give up your right to benefits while negotiations are ongoing throughout.

Will accepting a settlement affect my Medicare benefits?

Large settlements may be required to have Medicare Set-Aside arrangements. These help to protect Medicare’s interests in your case for the future. Failure to properly address Medicare can cause big problems. Consult with an attorney who knows the Medicare considerations before finalizing any settlement agreement.

Can I reopen my case after accepting a settlement?

Compromise and Release settlements usually close cases for good and all. You cannot reopen once you sign this type of agreement. Stipulated Findings settlements may provide for limited reopening for worsening conditions. Understand your type of settlement very well before you sign any final documents.

![Compliant Drivers Program: Is It Legit for Driver Safety? [2025]](https://propinfo.site/wp-content/uploads/2025/12/Compliant-Drivers-Program-150x150.jpg)

Leave a Reply