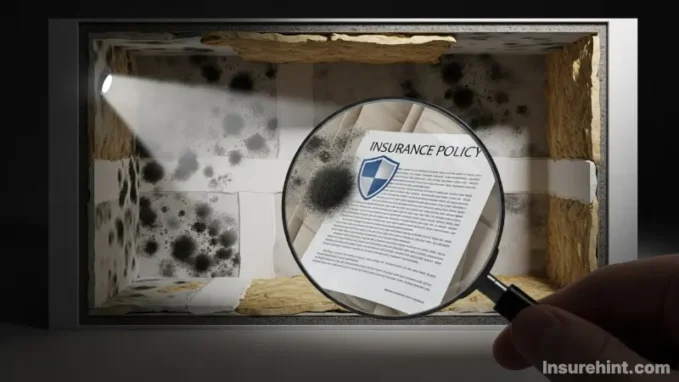

You can smell something musty in your basement. Then, you notice a dark ugly patch spreading on the drywall. Mold has officially invaded your home though. Your first thought is panic. Your second is a very important question. Does homeowners insurance cover mold?

This is one of the most common and confusing questions of home owners. The answer to this is not a simple yes or no. Instead, it is almost always “it depends.” Coverage is entirely dependent on where the moisture that caused the mold to grow in the first place is deriving from.

As a result, the process of knowing your policy can be like a maze. But don’t worry. We are here to help you know the details.

This will be a breakdown of everything for you. We will look into the time when mold is covered and when it is not covered. We will also discuss there being policy limits, renters insurance and proactive paces you can take as well. Towards the end, you will be a master on this complex subject.

Understanding Mold: A Homeowner’s Unwanted Guest

Mold is not just an unattractive stain, as well. It is a kind of fungus which can grow almost everywhere. It only requires moisture and an organic surface to grow. This includes wood, drywall, carpet and even dust.

Unfortunately, a small spot of mold does not take long to grow. It airborne releases spores in the air. These spores are likely to travel all over your home. This begins to form new colonies and it can affect the air quality of your home.

Some types of mold can be hazardous to one’s health. According to the Environmental Protection Agency (EPA) exposure to allergens is possible. It also may cause asthma attacks and other respiratory problems. This makes swift action a crucial effort.

Therefore, it is important to address the root cause of the moisture. Simply getting the surfaces where you can see mold cleaned is not enough. If the water source is still there the mold will almost certainly come back. This is the reason that insurance companies are so specific about it.

Why Insurers Are Cautious About Mold Claims

Insurance companies consider mold to be a major risk. Remediation can be extremely costly. It’s often not simply cleaning up the mold it’s replacing drywall, flooring and structures.

Furthermore, mold is usually a symptom of another problem. It is often a good sign of longer problems such as a slow leak, poor ventilation or general lack of maintenance. Insurers view these problems as avoidable maintenance problems.

As a result, standard homeowners policies have gotten very strict. Most are now containing specific language in them that is limiting or excluding mold coverage. They desire to cover sudden disasters, not the slow decay. Understanding this mindset is the first step to a good understanding of your policy.

The Big Question: Does Homeowners Insurance Cover Mold?

So, let’s find out about the crux of the matter. The answer to does homeowners insurance cover mold is found in the so-called “covered peril” rule. In insurance terms a peril is a particular event that results in a loss.

Damage caused by specific perils is covered under a standard policy. These include fire, lightning, wind storms and theft. If there was a covered peril which resulted in water damage, and that water damage resulted in mold, your policy will probably cover the mold removal of the mold.

The key words to zoom in on here is “sudden and accidental.” The water damage must be as a result of an unexpected event. Think of the bursting of a pipe, suddenly. This is far from similar to the drip of water that happens slowly over a period of months from a pipe.

“Coverages for mold are almost never related to the mold. It’s the event that resulted in the mold you all. If you have a chance when there is a source event that is covered, you have a really good chance. If this is not the case, you are probably on your own.” – Insurance Claims Adjuster

The “Sudden and Accidental” Rule in Action

Imagine that your washing machine supply hose was to suddenly break. It floods your laundry room. You wipe down the water that you just cleaned but one week later, you discover mold growing behind the base boards.

In this case, does home insurance cover mold? Most likely, yes. The cause was a sudden and accidental happening. The bursting hose is a covered peril. The resulting water damage and the subsequent mold is therefore covered.

Now, suppose it is another situation. You have had a slow persistent leak in your bathroom sink. You’ve ignored it for months. Eventually the mold grows and rots the whole cabinet and floor.

Here, the insurer will probably refuse to make payment. The damage was not sudden. It was due to a gradual leak and absence of maintenance that it happened. This is considered homeowner negligence which is a common exclusion.

Examples of Covered Perils That Lead to Mold

To make it more understandable, let’s examine certain situations. The policy is likely to cover mold in the event of one of these events.

- Burst Pipes: A Frozen Pipe Thaws and Bursts. This results in heavy water damage that results in mold.

- Appliance Malfunctions: Dishwasher or Ice Maker Sudden Line Leakage. This is a fairly common problem and has been covered in many cases.

- Fire Extinguishing: Firefighters use water to extinguish those fires in your house. The moisture left then causes the mold growth.

- Roof Damage from a Storm: A bad storm rips shingles off your roof. Rain gets in and causes mold. The initial damage was to be due to covered peril (the storm).

In all these cases, the water damage was an immediate result. It was not a long-term and predictable issue. As such the resulting mold is included in the covered loss. For complex policies, knowledge of options such as State Farm life insurance that can provide general financial protection as well will be helpful.

🏠 Mold Coverage: What’s Covered vs. Excluded 🔍

Common Exclusions: When You’re On Your Own

It is just as important to know when you are not covered. Insurance companies are very clear with these exclusions. Your reading your policy carefully is the only way that you can be sure. However, there are some common themes.

The biggest reason of denial is negligence. Insurance is supposed to be for accidents, not for things that you could have prevented. If you do not take care of your property you will probably end up paying for mold remediation out of your pocket. For business owners it is extremely important to find affordable business insurance to handle similar operational risks.

Negligence and Poor Maintenance

This is the most common cause of the denied mold claim. Insurance companies are expecting you to conduct regular maintenance. This includes repairs to leaky faucets and repair of cracked seals around windows.

For example, if you know your roof has old curling shingles and you don’t replace them, if that leads to a leak on your roof the leak is your fault. The insurance company will claim that the damage was predictable. Therefore, the problem of mold that you get is your financial responsibility.

Another example is a condensation problem on windows. If you don’t control the indoor humidity and you have mold growing on the sills then that’s a maintenance problem. It is not an abrupt and accidental occurrence.

Flood-Related Mold

This is a very important difference. Standard homeowners policies do not cover floods. A flood is defined as the cover of featuring water from a natural source, that is dry under normal circumstances. This includes overflowing rivers, storm surges or heavy rainfall.

If your home does flood and mold grows as a result your homeowners policy will not pay for it. You need such an insurance policy separate from the National Flood Insurance Program (NFIP) or a private insurance company. And without it you pay all expenses.

Reading the Fine Print: Mold Sublimits and Endorsements

Even when does homeowners insurance cover mold, the coverage is usually limited. Within the last 20 years or so, most insurers have added “sublimits” for mold. This is a limit on the amount they will pay for mold remediation.

A normal mold sublimit is between $5,000 to $10,000. This amount is for the total cost. It involves testing, remediation and repair. Unfortunately, a significant mold problem can easily be over $F & A costing more than this amount.

Suppose a burst pipe does $25,000 worth of damages. Of that $15,000 is for mold remediation. If your sublimit is $10,000 then the insurer will only pay that amount for the mold. You would bear the other $5,000 for mold, though they would pay for the other water damage.

For added protection there are some cases where you can purchase a mold endorsement. This is also called a rider. It gives you a further limit of your coverage for mold. This adds to your premium however, and is sometimes worth it, especially if you live in a humid climate. In the same fashion, Term life insurance vs whole life insurance helps you to make the right financial safety net choice.

What About Renters? Does Renters Insurance Cover Mold?

It is not only homeowners who have a mold dilemma. Renters face this issue too. The question then becomes, does renters insurance cover mold? The answer is similar but there are a few key differences.

Renters insurance mostly insures your personal belongings. It also insures against liability. It does not cover the physical building. That is the responsibility of the landlord.

So then, insurance renters will pay for the mold damage. It will include damage to your personal property. However, the same “sudden and accidental” rule applies. The resulting mold must put forth a covered peril.

For example, a pipe breaks in the wall of your apartment. It damages your furniture, clothes and electrons. It also causes mold to grow on those things. Your renters policy would likely cover the cost to replace your damaged things.

Landlord’s Responsibility vs. Tenant’s Coverage

The key is to be able to transform your property into something separate from the actual physical structure of the building. If mold grows on the drywall then that is your landlord’s problem. Their property insurance is to take care of the remediation of the building itself.

However, does renters insurance cover mold damage to your couch that was soaked in the process? Yes, it likely does. Now your stuff is safe thanks to your policy. Your landlord’s policy is for the protection of the apartment.

The situation becomes tricky if the mold is your fault by your negligence. For instance, say you made a bathtub overflow and it damaged the floor and your property, your liability coverage may be applicable for the floor. But, your home owner’s insurance policy might deny the part of the claim that the mold grew on your things, because you didn’t dry your things.

Therefore, the question do renters insurance cover mold really has two parts. It can cover your personal items in the event a covered peril is the cause. But, it will not be a treatment of the walls or floors of the apartment. It is also important to always communicate to your landlord if you have any water issues right off.

Mold During Construction: A Look at Builders Risk Insurance

Construction sites, including water damage and mold are uniquely vulnerable to water damage and mold. Exposed materials and open structures are easily susceptible to moisture. This brings up another area of insurance, builders risk.

A builders risk insurance policy is formulated to help in the protection of a building during its construction. Damage to the structure and materials on-site are covered by it. However, what should builders risk insurance cover in terms of mold?

Typically a standard builders risk insurance policy has little or no mold coverage. Just like a homeowners policy, it has often very specific exclusions to their policy. Mold is considered a preventable issue because of proper site management.

However, contractors can often have access to a mold coverage endorsement. This provides some molding protection for mold cleanup and remediation in the event of mold growth from a covered event, such as, for example, a heavy rainstorm that is too much of a load for a temporary roof. A good builders risk insurance quote will make it clear what these are.

Key Aspects of Builders Risk and Mold

When thinking about mold and new construction three points are very important. The builders risk insurance definition is one that covers a structure under construction. Its purpose is to provide protection to the investment until the project is done.

The cost of risk insurance for builders differs greatly. This depends on the value of the project, location, duration, and type of construction. The use of a builders risk insurance cost calculator may provide a rough estimate but a formal quote is required.

One of the major questions is who pays for builders risk insurance. Many times, it would be the general contractor. However, the property owner may be obligated by the contract of construction to purchase it. Clear communication is vital to ensure that there are no gaps in coverage.

The best approach, in the end, will be preventing mold during construction. This includes prevention of materials by staying dry and taking active water management. This is a lot cheaper than having to deal with a mold problem in an almost completed building. Similarly, having the right professional liability insurance is very important for contractors to manage his risks.

💧 Found Water? Your 5-Step Action Plan 🚨

🛑 Step 1: Stop the Water

Immediately find and shut off the water source. If it’s a major leak, turn off the main water valve to your house.

📋 Step 2: Document Everything

Take photos and videos of the leak’s source and all affected areas. This evidence is critical for your insurance claim.

🏢 Step 3: Notify Your Insurer

Call your agent as soon as possible. Explain what happened clearly and factually. Do not delay this step.

🔧 Step 4: Mitigate Damage

Start removing water. Use fans and dehumidifiers to dry the area. This shows the insurer you’re taking responsible steps.

🏠 Step 5: Hire Professionals

For significant damage, call a water restoration company. They have the proper equipment to prevent mold growth effectively.

Your Proactive Mold Prevention Checklist

The combined solution to a mold issue is to never allow it to occur in the first place. You cannot easily have a better defense than proactive maintenance. It not only protects your home, but also helps your position to be reinforced should you ever need to make a claim.

Remember though, insurers search for evidence of neglect. A well maintained home is your best bet against one such finding. Counseling for the Child and Adolescent: Some simple, frequent chores that you can perform.

Regular Home Maintenance Tips

- Inspect for Leaks: Regularly check under sinks, around toilets, and nearest the appliances. If there are signs of moisture then Seals are not tight enough.

- Control Humidity: attracted exhaust fans andaturated bathrooms and kitchens. Have a basement and crawl space dehumidifier in mind. Keep indoor humidity below 50%.

- Maintain Your Roof: Shingles Looking Bad or Lost Have your roof inspected once in a year. Clean your gutters to avoid having clogged gutters.

- Check Seals and Caulking: Examine window/door seals. Re-caulk tubs and showers in order to prevent water from seeping into walls.

- Make sure that you have Proper Ventilation: You should ensure that your attic and your crawl spaces are properly ventilated. This aids in retaining moisture from escaping, instead of building up.

- Address Condensation: If you have noticed condensation around windows and/or pipes, determine why the issue exists. It could be a feature of high humidity or poor insulation.

Making these little changes will save you thousands of dollars. It’s a lot less expensive to change a worn out washer on a faucet than it is to fix a mold infested wall. Just like with your health, having a good coverage, like humana dental insurance is all about preventive care.

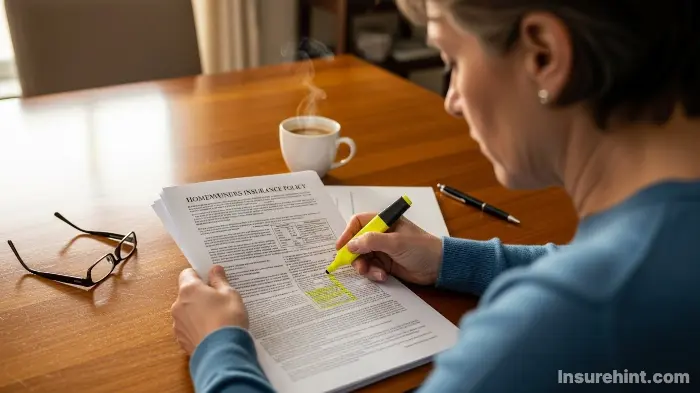

Navigating the Claims Process

Let’s say you have done everything right. A covered peril occurs and now you have a mold problem. Making the claim properly should be your next important step. How you deal with this process is an important factor in allowing you to impact the outcome.

Step-by-Step Guide to Filing a Mold Claim

First, act quickly. Mold may start to grow in as little as 24 to 48 hours of getting exposed to water. The longer you wait the worse the problem. The creditor could also find a way to suit you by saying that you didn’t do enough to mitigate the damage.

“The golden rule on water damage noted Mills Water in 1983 is “document, document, document.” The second you are looking at water your new job is to be a historian. There is no better tool in the claims process than your phone’s camera.” – Public Insurance Adjuster

- Review Your Policy: Before you even call, assume you have your policy pulled out. Try looking for sections which deal with water damage and specific mould cover/sub-exclusions. The power of knowing your coverage.

- Document the Damage: Take plenty of photos and videos. Catch the source of the water and everything impacted by the water. Don’t move or throw anything away without first seeing it by the adjuster.

- Call Your Insurer: Report the insurances claim immediately. Give the facts of what is what happened. Be honest and specific. You will assigned a claim number as well as an adjuster.

- Mitigate Further Damage: The clause in your policy is that you must take reasonable steps to prevent further damage. This means getting rid of standing water, using fans and getting undamaged property to a safe place. Keep receipts for any supplies that you buy.

- Get Estimates: Obtain estimates of the experienced mitigation companies of mold remediation. Your insurer might have a list of seven vendors they like to have material completed by, but you can get your own, too. This is important for knowing the whole scope and cost. Having a trusted insurer such as United Healthcare insurance for your health need is indicative of the value of having dependable partners.

What to Do if Your Claim is Denied

A claim denial is annoying, but it may not be the final word. First of all, you must know what exactly it was denied. Ask the insurer to give you a written explanation referring to specific language in your policy.

If you think that the denial is unfair, you have your options. You can appeal to the insurance company. Provide whatever other kind of documentation supports your case (e.g. a report from an independent contractor).

If the appeal is not successful, however, you may contact your state’s Department of Insurance. They are able to review your case and mediate in your behalf. As a last resort, you can hire a public adjuster or an attorney who specializes in doing insurance claims.

This process speaks to the different reasons why the first question, Does homeowners insurance cover mold is so complex. The answer frequently comes out of the details of a back-and-forth claims process. It’s not that policy, though: it’s the proof.

The Final Word on Mold Coverage

So and that being said, does homeowners insurance cover mold? Yes, but only in very certain narrow situations. Coverage is a side effect of some other covered event, rather than a feature in the product. It is associated with sudden and unexpected damage to water.

It will almost never cover mold from poor maintenance, long term leaks, high humidity and flooding. For these, the financial responsibility is in your hands, the homeowner, squarely in your hands. This is a difficult lesson for a lot of people to learn.

Your best that will insure against mold is not in the document of insurance. Underhand way no tool is in your toolbox. Nor in your schedule for maintenance. The leading is keeping the moisture at at. Routinely checking to see if there are leaks and controlling the level of humidity can prevent the overwhelming majority of mold issues.

At the end of the day, you need to read your policy today. Do not wait till you see a dark spot on your wall. Understand your sublimits. A mold endorsement can be purchased in order to provide you with more peace of mind. Being prepared is your great asset. It’s the same logic behind getting good temporary car insurance if you need it for a short time, or even having a good commercial auto insurance policy if you have a business fleet. Preparation is everything.

This can also include insurance types and the information on how you can support yourself in any budget and get cheaper, such as finding ways on how to get your cheap Car Insurance for the price lower. Whether you’re insuring your daily driver, your hobby automobile with classic motors insurance or even your two-wheeler with motorcycle insurance the details are important to know.

The complex question of does homeowners insurance cover mold does not have a simple answer. But, now you have the knowledge to save your home and your money.

Frequently Asked Questions (FAQs)

The cost ranges a lot depending on the extent of the problem. A small contained area could cost $500. A large scale remediation that is purely structural can easily cost upwards of $10,000-$30,000.

According to the EPA, if the amount of moldy area is less than approximately 10 square feet, you will be able to handle it on your own. Use protective attire as well as a solution of bleach or vinegar. For larger areas, it is always best to hire out.

For the mold to be SGC, it must be from a covered peril. This is called “Loss of Use” or “Additional Living Expenses” or ALE coverage. It helps to pay for hotel bills, meals while your home is getting repaired.

It’s possible. Any claim has the potential to result in an increase of the premium for your next renewal. However, a single claim, in particular for a clear covered peril, may not have a major impact. Another claim in a short period of time tends to increase your rates.

Mildew is a type of mold, very often gray or white, which has a powdery texture. It commonly grows in the surface of objects in damp conditions. Other molds can be black, green or yellow and can penetrate deeper into materials. Both of them are fungi and they need moisture to grow.

![Compliant Drivers Program: Is It Legit for Driver Safety? [2025]](https://propinfo.site/wp-content/uploads/2025/12/Compliant-Drivers-Program-150x150.jpg)

Leave a Reply