Imagine this, you live in your neighborhood and there is a sudden hail storm. You watch out your window as golf ball-sized ice puts dents in your new car. Who pays? The answer solely depends upon if you are selected Comprehensive Car Insurance or just the legal minimum. This difference isn’t a checkmark to check, but a difference between whether you can be saving for your financial future in case of the unexpected.

Your car is one of your most important possessions. Protecting it the right way is very important.

We’re here to penetrate the wall of literature that seems to be so confusing when it comes to insurance. We’ll talk you through the critical choice about these 2 core types of coverage. At the end you will know exactly what you need.

What is Third Party Car Insurance?

Let us begin with the absolute basics. So in what exactly third party car insurance?

This is the most basic level of auto insurance. In fact, it is the legal minimum requirement in almost every state. This is to defend other people against you.

Think of it this way; “third party” is the person you hit. The first party is you and the second party is your insurance company. This policy includes the damages of the third party.

It does not embrace your very own auto or your very own issues. It’s purely for the liability you have towards other people in an accident you cause. It saves you from incurring huge out of pocket expenses for someone else’s bills.

The Bare Minimum: What Does It Actually Cover?

So, what are you paying for with an insurance policy of basic liability? It’s broken down into two major parts.

First of all, you have the Bodily Injury Liability. This includes medical bills, lost wages and pain and suffering of people you injure in an accident when you are at fault.

Second, there is Property Damage Liability. This is to pay for repair or replacement of the other person’s vehicle or any other property that you damage, such as a fence or a mailbox.

There it is, a safety net, but a very basic one.

What is Comprehensive Car Insurance?

Now however, let’s change the gears to the next degree of protection. What Does Comprehensive Car Insurance Mean?

This coverage is totally different. It is not about accidents that you are causing.

Instead it helps protect your car from damages which are not collision related. Rather think of it as “other than collision” coverage. It’s the policy which comes in for all the random unpredictable stuff that life throws at your vehicle.

Such as theft, vandalism or fire or falling objects. It also includes natural disasters such as floods, hail or even hitting an animal such as a deer. Essentially, it’s your car covered when its sitting there just waiting to drunk, or not per se.

“Acts of God” and Other Unseen Events

The term “Acts of God” gets used a lot here. It sounds dramatic, but it simply means events that cannot controlled by man.

A windstorm that knocks a tree branch on your car is another perfect example. Another is a flash flood that struggles your automobile underwater.

This is the point where you see the true value of this coverage. It’s an extreme peace of mind service. You know that even if your car is stolen or damaged in some freak event of nature, you’ll not totally financially destroyed.

Expert Quote: The purpose of insurance has been said perfectly well by Dave Ramsey, a financial guru – “The purpose of insurance is to transfer risk.” You want to self insure the small stuff, and insure the big stuff. A totaled car definitely is big stuff.

The Critical Difference: Comprehensive Insurance Explained

So, what is the essence of all encompassing insurance?

The most important message to take away is that with comprehensive insurance you pay to repair or replace your own car after a covered non collision event. It’s all about saving your investment on your vehicle.

However, it is rarely sold from a stand-alone. It’s almost always covered with collision coverage. This duo is what most people are referring to as ‘full coverage’ and a term that offers a robust shield for your vehicle.

Collision Coverage: The Other Half of the “Full Coverage” Puzzle

Collision coverage is the other vital part. It pays to have your car repaired whether you are in an accident with other vehicles or objects, whether you were at fault or not.

This can be hits on another car, backing into a pole or a rollover accident.

When you combine Collision with a Comprehensive Car Insurance policy you have a powerful insurance coverage. This combination is normally mandatory from lenders if you have a loan or lease in your car. They would like to protect their financial interest in the car and this coverage can assure it.

Analyzing the Cost: Why is There a Price Difference?

It’s no wonder that the more coverage you have the more you have to pay. But why?

Insurers charge for premiums according to risk. A liability-only policy is less of a risk for them. They have to pay out only if you cause an accident and hurt someone else.

With Comprehensive Car Insurance the risk pool is drastically increased. Now, the insurer faces the risk of becoming liable for stolen, vandalized, weathers, etc goods and more. This higher chance of claim resounds to a higher premium to you. Deductible another factor is your deductible?

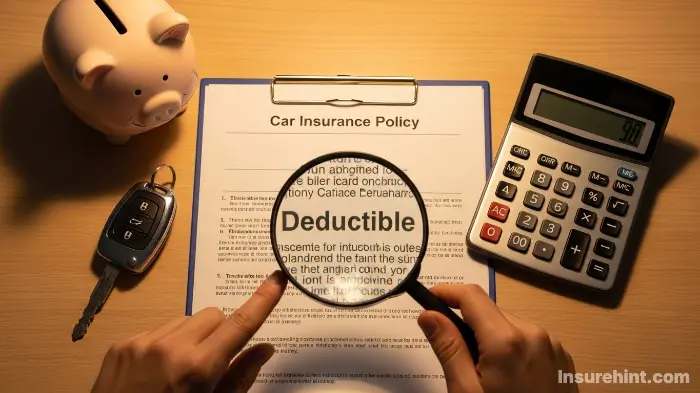

Understanding Your Deductible

A deductible is the amount of money you come to spend money out-of-pocket on a claim before your insurance will pay. Deductibles apply to comprehensive and collision coverage, but not to liability.

For example, bank to have your car covered with hail for $3,000 the following is how the insurance works for the cost: $3,000 $500 – the $500 is what you would pay first and the rest you will be reimbursed by the insurance company after you file an insurance claim. The remainder of the amount, $2,500, is then paid by your insurer.

Taking higher deductible is a common method to reduce the premium of your Comprehensive Car Insurance. You assume more initial risk, and in turn the insurer provides you with the better rate. Finding the right balance is the key to managing your overall car insurance cost.

Understanding Your Car Insurance Policy

It’s important to remember that your car insurance policy is a contract, which is divisible by law.

When you get your documents, don’t file them away. Labor the time to read your car insurance policy declarations page. It evaluates some real things, exactly what is covered, your limits your deductibles and any exclusions.

Many people are surprised to find out what is (and isn’t) covered after it has happened. Being aggressive about it and knowing what you are covered in from the first day can save you a lot of headaches later on.

Popular Add-ons to Consider

A standard policy is barely the beginning. You can customize your coverage with endorsements, or add-ons, to provide some coverage where it otherwise may lack.

Roadside Assistance is a popular one. It is useful in cases of lockouts, dead batteries and flat tires. Another is Rental Reimbursement. covers the expense of a rental car while yours is being repaired at the shop, following a claim on the covered vehicle.

Perhaps most important is Uninsured/Underinsured Motorist (UM/UIM) Coverage. This insures you should you hit by someone not being covered by insurance or not being covered by enough insurance. These add-ons greatly add to the Comprehensive Car Insurance plan, and create an even stronger safety net.

Real-World Scenarios: Who Pays for What?

Let’s make this crystal clear. We’ll run through a couple of situations you normally would see when these policies are run to see how they fare in real-world situations. Insurance works in ways that’s confusing and therefore experiences are best.

That way, you have insurance without personally understanding the actual value of a direct personal financial impact, this checklist will help you understand from your financial insurance choice to visualize direct.

Checklist: Who Pays the Bill?

Scenario 1: You run a red light and hit another car.

- ❌Your Car’s Damage: Not covered by either policy. (You need Collision).

- ✔️Other Driver’s Car/Injuries: Covered by your Third Party Liability.

Scenario 2: A deer jumps out and you hit it, damaging your front end.

- ✔️Your Car’s Damage: Covered by your Comprehensive policy (after your deductible).

- ❌Third Party Liability: Not applicable.

Scenario 3: Your car is stolen and never recovered.

- ✔️Value of Your Car: Covered by your Comprehensive policy (up to its Actual Cash Value, minus deductible).

- ❌Third Party Liability: Not applicable.

Is Comprehensive Car Insurance Always the Right Choice?

With all its advantages, you might wonder why not everybody have the Comprehensive Car Insurance? But that’s not always true.

The decision is highly individualistic. This depends on the value of your car, your financial circumstances and your willingness to risk it.

However, if you drive an old and high mileage car that won’t fetch much, the cost of the coverage may be more than offset by the potential payout. You could be spending a year’s worth of premiums more than your car is even worth. This is the situation when liability only might make more financial sense.

The 10% Rule: When to Consider Dropping Coverage

A very popular rule is the “10% rule.” It’s just a gut check of your coverage needs.

The rule is as follows: If the cost of your Comprehensive Car insurance and Collision coverage annual is more than 10% of your car’s cash value, then it could be time to consider trying to get rid of them.

For example, your car is worth $3,000. Your comprehensive coverage costs you $400 per year That’s over 10% ($300). In this case, you might be better off saving that premium money to repair the car later, or to put down on a new car. You can readily see how much your car’s worth on websites such as Kelley Blue Book (KBB).

Expert Quote: Suze Orman gives the advice of a practical approach, “If a car is a necessity then you have to have the proper insurance on it, that involves both liability and collision/comprehensive.” “I can live without that clunker” or “if it’s a piece of junk I don’t need.”

Navigating the Nuances of Third Party Liability Insurance

Even if you elect to go with the basic plan, there are some important details. The most important component of third party liability insurance is called your coverage limits.

When you buy your third party liability insurance if you look at it there will a whole set of numbers on it such as 25/50/25. This means $25,000 bodily injury on one person (and to one accident) and $50,000 or $25,000 property damage on accident.

While these may be your state’s minimums, they are often dangerously low in the modern day of high medical costs and expensive vehicles.

Why State Minimums Might Not Be Enough

Imagine that you cause an accident in which you total a $60,000 luxury SUV and send two people to the hospital.

If your property damage limit is only $25,000, you are personally responsible for the other $35,000 for the car. If there is more on their medical bills than your bodily injury limits, you could sued for the rest.

This is a sure trip to financial ruin. Experts at the Insurance Information Institute routinely advise carrying limits that are well over the state minimums (in some cases they recommend 100/300/100 or more to adequately protected). You may find out more about insurance definitions at Investopedia.

Special Cases: What About Leased or Financed Vehicles?

If you don’t own your car, then the choice is often made for you.

Nearly all auto lenders and leasing companies require you to have both Collision and Comprehensive Car Insurance. They are the legal owners of the vehicle until you pay off the vehicle.

They need to safeguard their asset. If the car is stolen or goes total the insurance company needs reassurance that their investment will returned by the insurance payout. Dropping this coverage would be a violation of your loan or lease contract.

GAP Insurance: Bridging the Financial “Gap”

This brings us to another important concept; GAP insurance. GAP is shorter for Guaranteed Asset Protection.

Cars depreciate quickly. It’s common to be in arrears on your loan amount than the car is actually worth, particularly over the first few years. This is referred to as being “upside-down.”

If your car is totaled, Comprehensive Car Insurance will only cover the Actual Cash Value (ACV) of the car. If you have a debt of $20,000 but the value of the car (ACV) is $16,000, then you’re left with an outstanding degree of $4,000 for a car that you don’t have anymore. GAP insurance helps to pay for that $4,000 “gap.”

How Your Vehicle Type Affects Your Insurance Choice

The make and model of your car has a vast effect on your insurance requirements. A brand new electric vehicle and even a 15-year outdated sedan have radically different needs.

Newer and more expensive cars almost always deserve complete coverage. The price to either repair or replace them is simply too much to risk.

If you own a special vehicle you may need a special policy. For example, insuring a vintage Mustang means you will need a specific classic car insurance policy and not a standard one. The same applies if you have the custom chopper which requires motorcycle insurance. The need for Comprehensive Car Insurance is almost a given for these high value assets.

Business Use and Your Personal Policy

Here’s an easy trap that costs a lot of money: Using your car for business.

Order in a standard auto policy clearly prohibits commercial use. If you’re a delivery driver, a real estate agent or rideshare driver.

If you have happen an accident while you are on the job, your claim will rejected. For these situations, you need a commercial auto insurance policy. This is a crucial difference for anyone whose running a small company or side hustle, it is part of the larger scope of your own business insurance strategy.

How to Get the Best Deal on Your Policy

Regardless of which coverage you go with, nobody wants to overpay. The good news is however, you have a lot of control!

The number one rule is to shop around. Get quotes from 3 to 5 different insurance companies at the minimum. There can be hundreds of dollars of variance for the exact same coverage.

Also, ask about bundling. If you have your auto policy bundled in with your home, renters, or even a State Farm life insurance policy, one of the great ways to get discounts is to combine them together. This may also be true with other policies as well, such as Humana dental insurance or even policies from other providers like United Healthcare insurance.

The Power of a Good Driving Record

The one single biggest factor that you are in control of is your driving record. A clean record with no accidents or tickets is like gold to the insurers.

It helps to prove to them that you are a low risk driver and they will reward you for that by offering you their best rates.

Many today’s insurance companies now have telematics programs (such as Snapshot from Progressive or Drive Safe & Save from State Farm). These incorporates a smartphone application or a small device to monitor you as you drive. Safe driving can result in significant discounts so that said, Comprehensive Car Insurance is much easier to afford.

Expert Quote: According to the Insurance Institute for Highway Safety (IIHS), “Vehicles with advanced driver assistance systems can lower claim rates for property damage,” which in turn can result in lower insurance premiums from insurance companies for drivers who opt for cars with advanced driver assistance systems.

What if You Need Coverage for a Short Time?

Standard 6 or 12 month policies don’t work in all circumstances. What if you only need insurance for a month?

This is where the non-standard policies come in. For example, if you are borrowing a friend’s car to take for a road trip or you’ve bought a car that you intend to sell in a few weeks, you might need temporary car insurance.

These policies cover valid periods for a short defined period. They guarantee you legally and financially are taken care without locking you to a long-term contract.

Other Insurance Types to Be Aware Of

Your car wouldn’t be the only asset that you have, and auto insurance wouldn’t be the only piece of your financial safety net.

As your life and career additional, your insurance need will too. A consultant may require professional liability insurance in order to protect them from liability claims that may be brought by clients who believe that they have suffered financial loss as a result of negligence. As you grow a family, comparing term life insurance becomes a number one priority. A well-rounded insurance portfolio will insure you from all sides. This third car insurance policy is often only the beginning.

The Claims Process: A Quick Overview

So, what happens when it is time to use your insurance? The process is very different.

With a third-party claim, the third party claims involves the other driver filing a claim against your policy. Locate your insurer copies your cat insurance and dedicates itself to communicate and pay for your behalf.

Filing Comprehensive Car Insurance claim is far more direct. You call your own insurance company and tell them about the damage (from theft, a storm, etc.), pay your deductible and they take care of the repairs. It’s a process that is for you not a third-party. A fourth good mix of comprehensive insurance is helpful here. The third third party car insurance policy place is clear.

What to Do After an Accident

No matter your type of coverage, for example, the steps taken after an incident are crucial. Obtain emotional distance (i.e., stay calm and have a plan of action).

First of all, be sure that everyone is safe. Move to a safe location if possible. Second, document everything. Take photos of all of the damage and the scene. Third, call the police in order to make an official report.

Last, contact your insurance agent or company, using false statements regarding the lead, as soon as possible. Having a good Comprehensive Car Insurance policy makes this very stressful process easier to get through, knowing that you have a team ready to help you get back on the road.

Conclusion: Your Peace of Mind is Worth the Protection

In the argument of Comprehensive Car Insurance vs. Third Party Liability, there’s no winner. The best option is the one that will suit your particular situation.

Third party liability insurance is your life’s blood, non-negotiable safety net that helps you avoid financially ruining other people. It’s the basis for responsible competitive driving.

Comprehensive Car Insurance on the other hand; is the armour that helps to protect your own asset. It’s for drivers whose vehicles are worth enough to pay for insurance against theft, weather and a world of other unknowns. Evaluate the value of your car, your money and your sanity. Then, you are free to choose the appropriate level of protection. Making an informed decision about your Comprehensive Car Insurance is one of the smartest financial decisions that a car owner can make.

Frequently Asked Questions (FAQ)

No, it does not. A comprehensive insurance form of car insurance will provide coverage for external events such as theft or weather damage. Mechanical failures such as a bad transmission or engine problems are considered maintenance problems and are not included in standard auto insurance. You’d have to get a separate mechanical breakdown insurance policy or a car warranty for that.

No, it is not. The only coverage that is required by law in most states is third party liability insurance. However, if you have a car loan or you are leasing out a car, your lender will almost certainly require you to have both comprehensive and collision coverage to protect their investment.

Yes, in many cases you can. This is sometimes known as “parked car” insurance. It’s an option for those people who want to store a vehicle alongside protection from theft, vandalism or weather without having to pay for collision. This does make sense for a project car or a vehicle that you don’t drive.

However, your location makes this huge. Insurers base their risk harm on your ZIP code. If you live in an area with high rates of auto theft, vandalism, or if you live in an area that is prone to severe weather events such as hail or flooding, you will pay more for your comprehensive insurance plan than someone in a lower-risk area.

It can but it’s generally less likely to result in a major rate increase in comparison to an at-fault collision claim. Claims for events totally out of your hands (hitting a deer, for example, or damage from hail) often are treated more leniently by insurers. However, a history of multiple comprehensive claims could result in a higher premium in the long run. This is a good aspect to look out for when you are looking for your car insurance policy. A third use of third party liability insurance is a good point of comparison here. A final use of third party car insurance and comprehensive insurance helps to meet the targets.

![Compliant Drivers Program: Is It Legit for Driver Safety? [2025]](https://propinfo.site/wp-content/uploads/2025/12/Compliant-Drivers-Program-150x150.jpg)

Leave a Reply