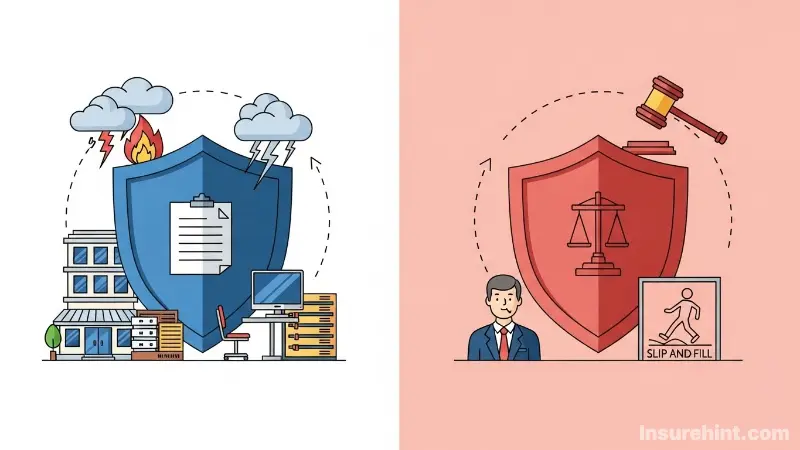

Starting a business is an exciting journey. You put your heart and soul into it. But what about protecting it? Insurance is a confusing topic. In fact, many business owners confuse two important policies. They confuse Commercial Property Insurance with general liability. But, these are not similar at all. Indeed, they protect your business very differently.

Consider them two separate shields. One protects your physical things and the other protects you from lawsuits. Understanding this difference is not merely smart. In reality, it is vital for you to survive. For this reason, this guide shall break it all down for you. We are going to keep it as simple and obvious as possible.

The Foundation of Business Insurance Protection

Before we deep dive let us first set the stage. Business insurance isn’t one product. Instead it is a package of policies. Each of the policies is designed to cover specific risks. You couldn’t for example fix a leaky pipe with a hammer. Likewise, you need the right insurance for the right risk.

For most businesses, protection consists of two areas. First, you have your property, your tangible assets. Second, you have your liability: your legal obligation to others. Both are critical. Consequently, to ignore one may result in a financial disaster. It’s a risk that’s simply are you have to just cannot afford to take.

A Deep Dive into Commercial Property Insurance Coverage

What Exactly is Commercial Property Insurance?

That can begin with your physical assets. Commercial Property Insurance, as its name implies, is the insurance policy that insures the “stuff” you own or rent. It is intended to pay for the repair or replacement of your property. This is applicable if it is damaged by a covered event.

Think through your business location. It could be an office, a storefront or a workshop. This policy serves to protect the building itself. Furthermore, it is also inclusive of everything within it. This includes your furniture, computers, and your inventory. Ultimately it is a safety net for your physical investments.

What Assets Does Commercial Property Insurance Cover?

This coverage is quite broad. In particular, it generally covers a number of the following key categories. Let’s look at what’s protected.

- The Building: This includes the physical building that you own.

- Your Contents: Desks, chairs and filing cabinets.

- Technology & Equipment: Computers & printers, specialized machinery: This one is obvious!

- Inventory: It safeguards the products that you have waiting to be sold.

- Exterior Fixtures: This can include your sign for your business or fencing.

- Others’ Property: If you hold the property of your customers, then it can be covered too.

Essentially, if it is a physical item that is vital to your business, this policy is probably covering it. You can even get coverage for things like valuable papers and records. Therefore, proper protection here is an integral part of a sound business plan.

Perils Covered by Commercial Property Insurance: The Two Policy Types

Just as all Commercial Property Insurance policies are not created equal. They come in two flavors usually. These are named-peril and open-peril policies. Of course, to understand them is very important.

Named-Peril Policies

A named-peril policy is very specific. It specifies what events (or “perils”) exactly are covered. An example of a frequent policy could be:

- Fire

- Theft

- Vandalism

- Windstorms

- Lightning

If a disaster does not make that list, then you are not covered. Therefore, these policies can be lower cost. But they get you left with more possible holes in your coverage as well.

Open-Peril Policies

An open-peril policy, on the other hand, works the other way. It excludes everything trespassing out save for that which it expressly excludes. This provides much more expansive protection. For this reason, the list of exclusions is very important. You must read it carefully.

Pay exclusion will also commonly include:

- Floods

- Earthquakes

- Acts of war

- Adult monkeys suffering damage that is intentionally caused by the owner

For most businesses, an open-peril policy is definitely the better option. It makes for more holistic security from unforeseen events.

“Risk-taking is the result of not knowing what you’re doing.”

– Warren Buffett

Who Needs Commercial Property Insurance for Their Business?

You would think that this is only for large corporations. That is a common mistake. In reality, nearly every business requires it.

- Business Owners: If you are the owner of your building, this is a must-have.

- Business Renters: Your landlord’s policy will not cover your business property. Thus you need a policy for your inventory, equipment and furniture.

- Landlords: If you lease out space, then you need your property insurance for rental property. This ensures that you are not risking investment in the building itself.

Even if you conduct business out of your home, do not count on your homeowners policy. Most have very limited business asset coverage. As a result, you probably will require a separate policy or a special endorsement. Exploring various plans, such as that offered by United Healthcare Insurance, demonstrate how specific needs necessitate for specific policies and it apply to all types of insurances.

Commercial Property Insurance

Focus: Protects your physical assets.

- Covers your building.

- Protects inventory & equipment.

- Triggered by physical damage (fire, theft).

- It’s about “what” happened to your stuff.

General Liability Insurance

Focus: Protects you from claims by others.

- Covers third-party injuries.

- Protects against property damage you cause.

- Triggered by a lawsuit or claim.

- It’s about “who” was harmed by your business.

Unpacking Commercial General Liability (CGL) Insurance

What is Commercial General Liability Insurance?

Let us now change gears to the other shield. Commercial general liability insurance (CGL): It is about what you do. It helps your business by protecting you from claims made by third parties. Incidentally, a third party is anyone other than your employee.

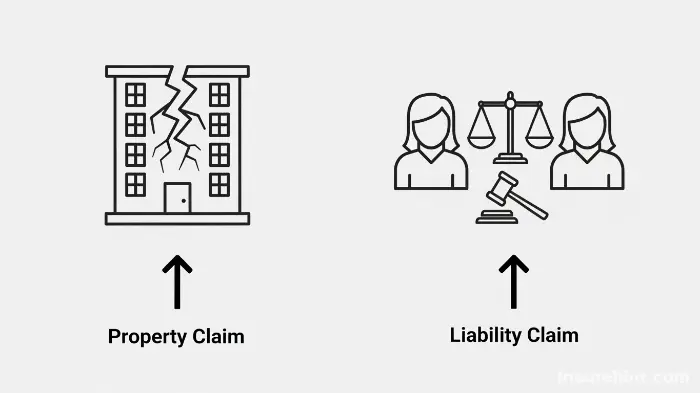

These claims are generally claims for bodily harm or a property claim. For example if the customer slips and falls in your store, CGL can help. It takes care of their medical bills and your legal defense expenses. Of crucial importance, it doesn’t protect your own property. This insulates you from liability to others.

Scenarios Where CGL Insurance is a Lifesaver

To get a good idea of CGL, it would be better to consider real life situations. To illustrate, let’s take some examples where this covering is very critical and important.

- Slip and Fall: A customer slips on the watered down floor of your cafe. They break their arm and file a lawsuit against you. CGL can cover their medical bill and your legal bill.

- Property Damage: Your landscaping workers accidentally break a client’s costly window. In this case, CGL can fund the replacement.

- Product Liability: You sell a toy that has a defect, which causes a child to be injured. CGL can then help to the resulting lawsuit and damages.

- Advertising Injury: You inadvertently use a copyright protected image in your advertising. The owner sues you. Again, CGL can cover the legal fallout.

Without commercial general liability insurance, any of these events could put your business out of business. Therefore, it is a non-negotiable policy for almost anybody. Even you are a freelancer, then you may require some coverage like professional liability insurance which is a cousin to CGL.

Key Components of a General Liability Policy

A standard CGL policy is based on a small number of basic coverages. Each one is addressed to a different form of risk you might be exposed to.

- Bodily Injury and Property Damage: This is the main part of the policy. It covers harm that you cause to other people or their property.

- Personal and Advertising Injury: This is the protection for the injuries which are not physical in nature. For example, allegations of libel, slander, or infringement of copyright.

- Medical Payments: This component can pay for minor injuries to a third party. It can be used no matter whose fault it is. Consequently, this can often stop a small problem from becoming a large lawsuit.

Understanding these components you can understand the complete protection this type of protection actually encompasses. In fact, it protects your business from many legal threats that are common.

What CGL Insurance Does Not Cover

It is just as important to know the limitations of CGL. This is not a policy that will cover everything. Moreover, knowing what it does not cover helps you to establish which other insurance you might need.

CGL generally does not cover:

- Damage to your own business property (that’s for Commercial Property Insurance).

- Injuries to your employees (this is covered by Workers Compensation Insurance).

- Professional errors or mistakes (that’s for Professional Liability/E&O Insurance).

- Auto accidents in a company vehicle (this requires commercial auto insurance).

- Where deliberate acts are harmful.

The Core Differences: Commercial Property Insurance vs. General Liability

So, we have seen both the policies. The great difference is simple but great. In short, it is all about: who and what is being protected. Let’s make it crystal clear.

Focus of Coverage: Business Property Protection vs. Theirs

Commercial Property Insurance is Inward Looking. It looks down your business, and to your assets. The focus on keeping safe to protect the things you own or are responsible for. It is all about your stuff.

Commercial general liability insurance, on the other hand, is facing outward. It takes into account how your business impacts others. The concern is to protect you against the claims of third parties. It is all about their stuff (or their well being).

Triggering a Claim: Physical Business Loss vs. Legal Action

The event that will begin a claim is also very different. A Commercial Property Insurance claim normally starts with a direct physical loss. For example, your warehouse is burned down by a fire. A storm damages your roof. Or maybe a thief steals your computers.

On the contrary, a CGL claim often begins with an accusation or lawsuit. A person alleges that you are responsible for their injury. A client accuses you of damaging their property. In this case, the trigger is a legal movement, not simply a physical movement.

“The first step in managing risk is to know what and where your risks are.”

– A.J. Korzeniowski

Combining Coverages: The Power of a BOP

At this point, you may be thinking to yourself “This is a lot to handle.” You are also probably realizing that you are in need of both policies. Most businesses do. After all, the risks they cover are distinct and just as important.

Luckily, we have insurers that have a solution. It’s known as a Business Owner’s Policy, or BOP.

What is a Business Owner’s Policy (BOP)?

A BOP is an almost package deal. It takes multiple essential coverages of insurance into one policy. Most BOPs put together three basic protections:

- Commercial Property Insurance

- Commercial general liability insurance

- Business Interruption Insurance (which covers lost income after a disaster)

Advantages of a Business Owner’s Policy

There are several benefits of choosing a BOP. As a result, it is a popular choice of small and medium-sized businesses.

- Cost-Effective: Bundling these policies is almost always cost-effective compared to purchasing them individually. Many people resort to similar strategies for personal policies, always seeking to learn tips for how to lower your insurance cost.

- Convenience: You are only dealing with one policy and one premium. This certainly makes your paperwork easier and your life easier.

- Comprehensive: it includes the most common risks that a small business may encounter. This helps to form a good strong foundation for protection.

However, it is not possible for all businesses to qualify for a BOP. They are generally for businesses in industries of lower risk. You also generally need to satisfy certain size and revenue specific requirements. Your insurance agent can tell you whether or not a BOP is right for you. Even if it isn’t, it is still possible to find affordable business insurance by working with a good agent.

Which Business Risk Shield Do You Need?

If you own or rent a physical space…

You need Commercial Property Insurance to protect the building and your contents.

If customers visit your location…

You need Commercial General Liability for slip-and-fall risks.

If you have inventory or equipment…

You need Commercial Property Insurance to cover theft or damage.

If you advertise or market your business…

You need Commercial General Liability for advertising injury claims.

Special Commercial Property Insurance Considerations

Insurance is not an individual one size fits all cover. The proper blend of the coverage owe to your discrete operation. For this reason, let’s take a look at some common types of businesses.

Home-Based Businesses

Running a business from home is very common. However, many owners assume disastrously. They think their homeowners’ insurance covers them. Unfortunately, that is often not the case. As this external resource from the U.S. Small Business Administration (SBA) points out, it is not uncommon for personal policies to exclude business activities.

Your homeowners’ policy may have a teeny tiny limit for business property in it. For instance, it might be just $2,500. Furthermore, a CGL claim would very likely be denied. You therefore need a separation of business policy.

Renters and Landlords: A Two-Sided Coin

The relationship of a landlord to a tenant brings out the insurance difference perfectly. Both parties require their own distinct covering.

The need to take out property insurance for rental property by a landlord. This helps protect their financial interest in the structure of the building. Additionally, they must have liability insurance in case their inattention (such as a poor staircase) has caused an injury.

The tenant, on the other hand, require Commercial Property Insurance for his/her own things. This includes their inventory, computers and furniture. They also absolutely need commercial general liability insurance for their daily operations. For instance, if a customer slips inside of his or her rented shop.

Service vs. Product-Based Businesses

Your business model also has an impact on your risks. Businesses selling products have considerable inventory. This is why Commercial Property Insurance is a high priority. They also have product liability risks covered by CGL. A State Farm life insurance protects your family’s future; just as CGL protects your business’s future from lawsuit.

A service-based business such as a consultant might have less physical property. The greatest danger that they face may be that they give bad advice. While CGL is still necessary to cover general risks, they should also strongly consider Professional Liability Insurance. This is designed accordingly for errors in professional services. The principle of specific coverage for specific needs is also seen in healthcare with Humana dental insurance plans.

How to Choose the Right Business Insurance Policies

Now you know what is the difference. The next step is getting the right coverage. It requires a little home work, but it is time well spent.

Assess Your Unique Business Risks

First, begin to think like an underwriter of insurance. Walk through your business operations. Then create a list of possible risks.

- What physical assets are most valuable?

- How much would it cost to replace it all?

- Do your customers visit your premises?

- Do you go to client sites?

- What are the probabilities of someone getting hurt?

This risk assessment will help to make your discussion with an insurance agent. In addition, it helps you know what you really should protect. This is similar to evaluating the need for other types of specialized coverage, such as for a classic car.

Working with an Independent Insurance Agent

You can buy insurance online. However, when it comes to business insurance, it is a good idea to work with an agent. Being an independent agent can be such a huge asset. This is because they are firearm insurance companies.

This means they can shop around for you. They may find the best coverage at the best possible price. An experienced agent will even assist you to find issues that you may have not thought about. In the end, they are an invaluable guide in this process. According to a study by Investopedia, it is possible to obtain better coverage and better pricing when using a broker.

Read the Fine Print: Understand Your Policy

Once you get a quote don’t just look at the price. You need to read the policy documents. Pay close attention to:

- Coverage Limits: Maximum amount to be paid by the insurance firm in response to a claim.

- Deductibles: The amount that you will need to pay for out of pocket before the insurance gets active.

- Exclusions: The list of said that are not* covered.

Understanding such details is crucial. Above all, it saves you the surprises if you have to proceed to file a claim. If it sounds complicated, tell you agent to help you understand it. That is what they are there for. Just the same decision of term life vs whole life insurance, the details matter immensely.

Conclusion: Two Essential Shields for Your Business

In the world of business, you are exposed to risks everyday. Some are financial and some physical. Commercial Property Insurance and commercial general liability insurance are two strong, separate safeguards that serve to protect you from these risks.

Commercial Property Insurance protects your physical kingdom: your building, your equipment, your inventory. In contrast, general liability protects the reputation and finances of your kingdom against attacks from outside: the lawsuits and claims of third parties.

“The future cannot be predicted, but it can be created.” The second-best way is to insure it.”

– Anonymous

Most businesses need both. One without the other leaves a gaping dangerous hole in your defenses. By understanding their differences, you should finally be able to make informed decisions. You can create an extensive insurance plan that allows you to do what you do best: run your business. So do not wait until a disaster occurs to find out there is a gap in your coverage.

Review your policies today. Talk to a professional and make sure that your hard work is well protected. Just like you would need special insurance for a motorcycle, your business needs your own special insurance. Even if you want to be covered only for a very brief period, options such as temporary car insurance demonstrate how flexible the market can be.

For more information on risk management, the Insurance Information Institute (III) provides a wealth of knowledge on general liability and other forms of coverages.

Frequently Asked Questions (FAQs)

For most businesses, this is not advisable. Commercial Property Insurance and General Liability have two completely different risks. Not having any is to be left by yourself. A Business Owner’s Policy (BOP) is a good option to bundle them.

You probably still need General Liability for such things as advertising injury (such as copyright claims). You may also need Commercial Property Insurance If You Have Significant Inventory or Computer Equipment that is Even Stored in your Home.

No. General Liability insures third-party bodily injury and property damage. In contrast, Professional liability (or E&O) relates to financial loss to a client as a result of your professional negligence, errors or omissions.

The cost varies greatly. Specifically, it depends on your building’s value, location (risk of fire, crime, etc.), construction type and the value of your business property.

No. The landlord’s policy covers on the building structure. It does not include your business contents (inventory, computers, furniture) and your liability for accidents occurring on your leased space. Therefore, you need policies of your own.

![Compliant Drivers Program: Is It Legit for Driver Safety? [2025]](https://propinfo.site/wp-content/uploads/2025/12/Compliant-Drivers-Program-150x150.jpg)

Leave a Reply